Since 9 August, the Unilever (LSE:ULVR) share charge has truly raised by 4% (at 30 August).

This is regardless of Trian Fund Management, the funding firm found by activist financier Nelson Peltz, unloading 3.82 m shares within the enterprise at a heavy typical charge of ₤ 47.33.

Peltz is moreover a supervisor of Unilever.

The sale produced ₤ 181m. But the reality that such a well-known quantity has truly chosen to reduce his holding doesn’t seem to have truly discouraged others from buying.

| Date of sale | Number of shares marketed | Average charge (₤) | Sales earnings (₤) |

|---|---|---|---|

| 9 August | 2,931,127 | 47.38 | 138,876,797 |

| 12 August | 738,471 | 47.19 | 34,848,446 |

| 13 August | 155,000 | 47.11 | 7,302,050 |

| Totals | 3,824,598 | 47.33 | 181,027,293 |

The information to the inventory market actually didn’t provide any kind of concepts concerning the components behind the sale. It barely describes “portfolio management” as the important thing inspiration.

But because the claiming goes, somebody’s rubbish is a further’s prize. The enterprise’s share charge has truly been pressed higher as financiers– not resenting the sale– need an merchandise of the sturdy items titan.

A earlier investor

I made use of to have a threat inUnilever But I obtained aggravated because the share charge appeared not capable of seem the ₤ 43-barrier.

Since after that it’s climbed by about 14%. Despite this, I don’t be sorry for advertising– I’ve truly finished a lot better some other place.

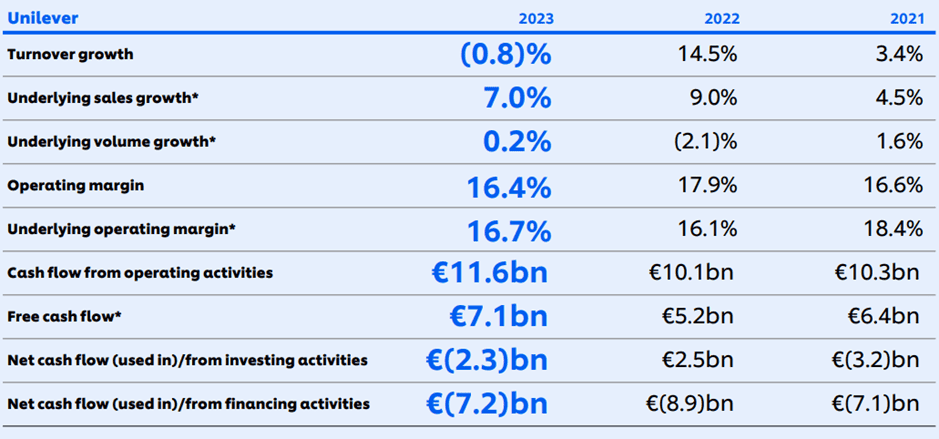

However, Unilever is a fine quality enterprise with a exceptional profile of home model names. It regularly produces EUR10bn-EUR11bn of money cash from its working duties.

Its outcomes for the very first 6 months of 2024 disclosed gross sales growth, each with regard to charge and amount. And its working margin enhanced.

This success is credited to concentrating on the enterprise’s main 30 model names, which make up round 75% of flip over.

The workforce’s continuing stable effectivity calls into query the idea that clients are coming to be considerably charge delicate and exchanging better-known names for inexpensive choices.

But undoubtedly there’s reached come an element when it’s no extra possible to raise prices with out dangerous revenues?

I cannot suppose precisely how expensive just a few of Unilever’s objects have truly ended up being, particularly when contrasted to a number of grocery retailer own-brands. Personally, I assume we could possibly be close to ‘peak prices’ for a lot of its objects.

Too costly

Similarly, I assume the enterprise’s shares are expensive.

Analysts are anticipating hidden revenues per share of EUR2.76 (₤ 2.33) for the yr ending 31 December 2024. This suggests aforward price-to-earnings ratio of around 21 This will get on the excessive facet, additionally for a participant of the FTSE 100

And it’s considerably over its five-year commonplace.

Nor does the provision present up to make use of nice value when contrasted to that of, as an illustration, Reckit Benckiser, which trades on an onward quite a few of 13.7.

Underwhelming returns

Unilever’s returns is moreover irritating.

In 2023, the enterprise paid 148.45 p a share. If duplicated this yr, it suggests acurrent yield of 3% For a income financier like me, that’s inadequate, particularly from a agency that’s one thing of an atm.

When I initially bought the provision, it was producing close to the Footsie commonplace of three.8%. For higher distinction, Reckit Benckiser’s provide is presently supplying a return of 4.4%.

It’s for these components– questions over its functionality to raise prices higher, a toppy evaluation, and a parsimonious returns– that I don’t intend to spend.