Looking for returns improvement provides? These FTSE 100 provides are anticipated to supply stable fee improvement over the next variety of years a minimal of.

BACHELOR’S DEGREE Systems

Dividend return: 2.5% for 2024, 2.7% for 2025

The regular nature of arms prices implies assist typically tends to be a well-founded discipline fordividends This is especially the scenario at this time, as cracks within the worldwide order drive fast rearmament within the West.

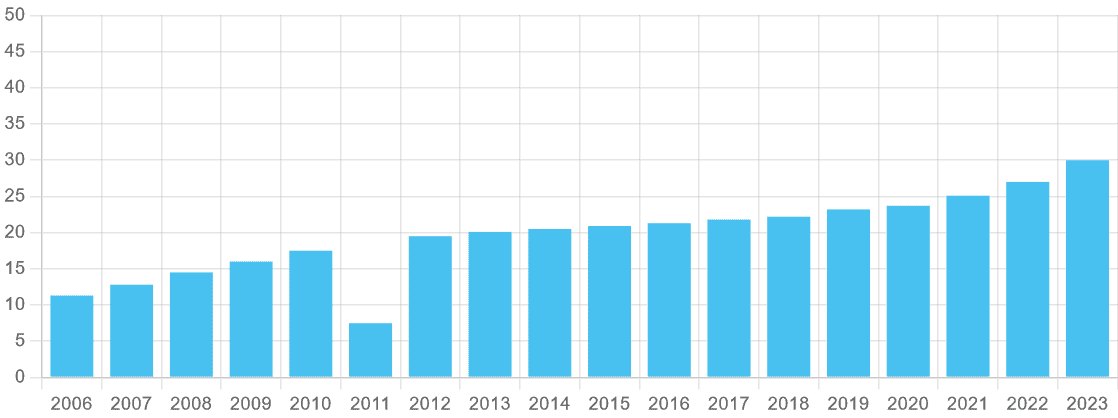

BACHELOR’S DEGREE Systems (LSE:BA.) is one service supplier with a prolonged doc of notable returns improvement. It’s elevated investor funds yearly contemplating that 2011. It’s a fad City consultants anticipate to proceed, making it price a detailed search in my perspective.

Payouts are anticipated to climb 8%, to 32.3 p per share, this 12 months. Dividend improvement is anticipated to extend to 10% in 2025, resulting in a full-year fee of 35.5 p.

Forecasts for following 12 months are sustained by anticipated earnings will increase of seven% and 12% in 2024 and 2025 particularly. As an impact, approximated returns for each years are coated 2.1 occasions by anticipated incomes.

Both analyses are over the protection and safety standards of two occasions, providing returns projections with added metal.

BAE moreover has stable financial constructions to cash returns in scenario incomes dissatisfy. Profits would possibly disappoint value quotes due to present chain issues, for instance, a considerable hazard to assist corporations’ yearly incomes at this time.

The Footsie firm had ₤ 2.8 bn of cash on the annual report since June.

BACHELOR’S DEGREE Systems’ order stockpile is rising, and it struck a doc ₤ 74.1 bn on the center of 2025. It seems to be readied to keep up climbing as nicely, which bodes nicely for longer-term returns.

Airtel Africa

Dividend return: 5.4% for 2025, 5.5% for 2026

Telecoms provider Airtel Africa (LSE:AAF) doesn’t have a prolonged doc of returns improvement like BAE. It’s simply been supplied on the London Stock Exchange for five years. It moreover lowered the yearly fee in 2021 because it rebased returns to cut back monetary obligation.

However, cash funds have really risen ever since, and by larger than double-digit parts occasionally. It’s a fad that City brokers anticipate to proceed.

For this fiscal 12 months (to March 2025), a whole returns of 6.52 United States cents per share is anticipated, up 10% 12 months on 12 months. An further 3% enhance is predicted for financial 2026, to six.70 cents.

However, I must advise that Airtel’s projections aren’t as sturdy as I ‘d ideally resembling.

Profits are skidding lowered due to detrimental cash motions (EBITDA went down 16.5% in between April and September). And make the most of levels are dramatically increasing, with net-debt-to-EBITDA climbing to 2.3 occasions since September.

Falling incomes moreover suggest returns cowl transforms adversarial for this 12 months, with anticipated incomes of 46.7 United States cents per share projection. On the plus aspect, City consultants anticipate earnings to rebound extremely in financial 2026, leaving sturdy returns cowl of two.7 occasions.

Yet whatever the unclear near-term overview, I nonetheless assume Airtel Africa shares deserve main issue to contemplate by risk-tolerant capitalists.

What’s further, I believe the lasting picture proper right here stays very interesting. Telecoms want for Africa stays to rocket, with Airtel’s client base climbing 6.1% 12 months on 12 months to 156.6 m in September.